Are you providing the experiences your customers are looking for through retail digital banking transformation?Imagine it’s a customer’s lunch break. She has 60 minutes to get some food, eat, and unwind before getting back to work. Let’s say this customer also needs to deposit a check during her break since after-work commitments are preventing her from getting it done on the way home. Does she willingly give up her lunch to head to the bank and risk spending 60 minutes standing in line? Or would she rather visit her bank’s mobile app, take a photo of her check and deposit it within seconds?It’s not a difficult choice—especially for today’s digitally savvy consumers. These consumers do not like standing in line or guessing how long a transaction will take. They also shop more online, and expect excellent customer experience services and instant gratification.The problem is that most non-digital retail banks only seem to offer long lines, and tons of paperwork. Customers who visit a traditional bank will be lucky to leave within an hour and a half just to open up a savings account.

Appealing to the on-the-go customer

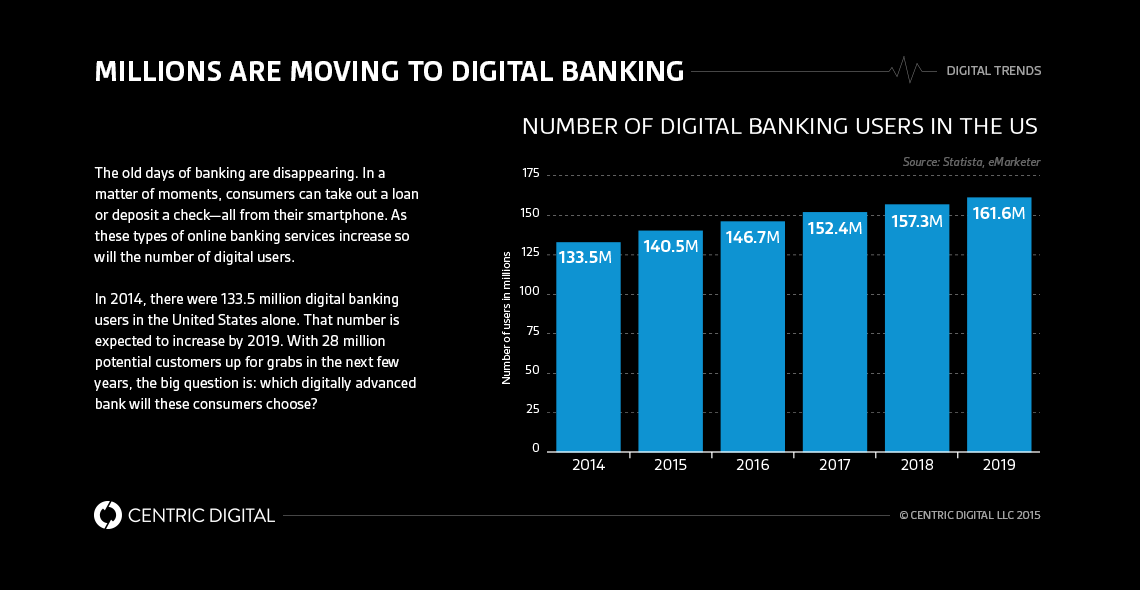

Right now, we’re witnessing a big shift in retail digital banking with remote deposit capture. According to CBS News, more than half of today’s mobile banking users have used their smartphones to deposit checks, compared to 38 percent in 2013. Customers no longer have the time or inclination to visit a bank to do something they can just as easily do through an app.Millennials and the preceding generations will also become increasingly unfamiliar with visiting a physical bank branch. Instead, they’ll want to know how to manage financials, transfer money, and even apply for credit by visiting a website or using a mobile app. As the world becomes increasingly digitized, more and more users will be heading in this direction. Their lives are on-the-go, and the banking industry must be able to keep pace.As users demand more digital experiences that will save them time and stress, it’s clear that the old ways of banking must change. The transformation of digital services in banking just makes sense—not only from a time-saving standpoint, but from a customer-demand standpoint as well.However, banks won’t be able to simply create a few mobile apps and call it a day. The full digital transformation of banking needs to be as innovative and customer-centric as the digital movement itself.

Providing digital innovations to serve all customers

Bank of America has made big moves to adopt digital change within their own branches—and they’ve also included digital experiences for their customers outside of mobile apps. Their latest big step forward is the new Teller Assist service, which is an ATM that connects you via a video conference with a remote teller. Customers can perform simple ATM functions with Teller Assist, as well as more complex transactions—eliminating the need to stand in line and wait to be called over by the next available teller.This service has saved bank-goers tons of time and also improved the limited hours that banks are open. Teller Assist provides users with extended banking times that are not restricted by a building location’s hours of operation.

Avoiding bank hopping

In addition to demanding more mobile and digital experiences, today’s consumers are also hopping between banks more frequently than ever before.Customers are switching between vendors, carriers, and/or banks—and it’s not just due to price, but also convenience. They’re looking for the bank that will provide them with the best customer experience to meet their needs.By enacting a retail digital banking transformation, you can appeal to on-the-go bankers and new generations of digitally savvy consumers, while also maintaining your existing client base. If not, then digital companies or other forward-thinking banking institutes will be in a prime position to eliminate the competition.

Contact Us

Centric Digital is no longer active. This site is preserved as an archive. For inquiries, please fill out the form.

© Centric Digital 2025