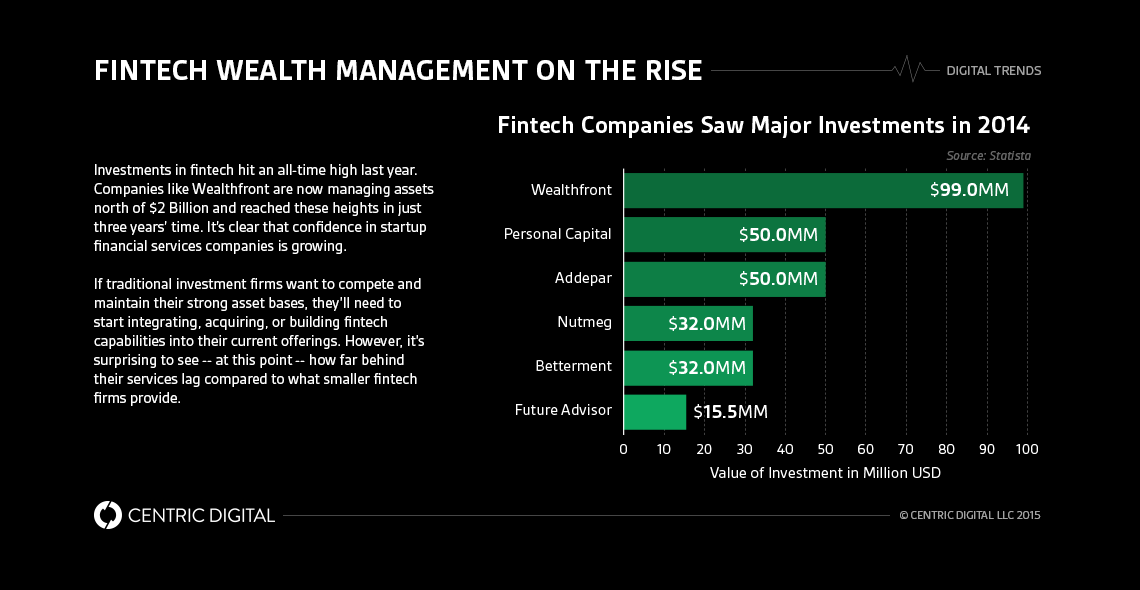

Since the launch of Etrade, traditional wealth management firms like Morgan Stanley, Merrill Lynch, and even the more consumer friendly Fidelity and Schwab have been either too resistant or too slow to provide similar capabilities that disruptive startups have brought to consumers. Automated investment management’s rise in popularity but stagnation in traditional companies is yet another example of what they could and should provide through digital.I’ve been investing in the stock market since the pre-online trading days. I have used every firm from all the variations of Smith Barney -- now integrated into Morgan Stanley -- to Etrade and even the early social investing platform Covestor. Ultimately, I found most services’ best practices lagged behind what was possible in digital experience and capabilities.More recently, I’m using several fintech disruptors like SigFig (and its previous iteration, WikInvest) to get a better portfolio data visualization. And I have experimented with a new guard of automated investing tools like Betterment and Personal Capital for alternative approaches to investing.So why the shift towards the disruptors and away from the old guard? Let’s take a closer look.

A Generational Change

Events like the collapse of Lehman Brothers and the Madoff investment scandal have shaken the confidence of baby boomers and Generation X investors in even the most stable wealth management firms. That means the most beautiful data visualization in the world won’t inspire confidence if the track record is less than a decade long -- and yet, investors do want these capabilities.By the same token, it’s not surprising that traditional stockbrokers may decry these services as big risks or only useful for small accounts. Many, though, are probably more concerned by the threat of transparency, low fees, and potentially better performance with less effort these automated services offer. It’s equally unsurprising that some traditional management companies and their executives have relied on these excuses to avoid the need to transform their business model and provide similar digital capabilities.However, as older generations entrust their wealth management to their children, the pressure on traditional management companies to provide these capabilities will continue to mount. Accustomed to more control, transparency, and digital visualization, Generation X and millennials will demand these features in their asset management. Coupled with the trend and acceptance of more passive or automated investment over manual custom portfolio management, more people will seek out the capabilities that the likes of SigFig, Betterment and Personal Capital provide.

Steps in the Right Direction

So I was excited the other day to receive an email from SigFig promoting their integration and capability to manage Fidelity accounts. This combines what is currently the best of both worlds: the security of having your assets at a stable financial institution with the cutting-edge data visualization and investment automation capabilities of a fintech startup. Fidelity has already made its own steps towards investing in fintech in Boston through a program called the Fintech Sandbox, but this represents another step forward entirely.Similar to how some traditional banks are embracing fintech in different ways, traditional management companies need to find ways to proactively engage (and possibly acquire and/or integrate) these emerging companies’ capabilities. Better yet, they could step up their digital transformation efforts and build these capabilities into their existing platforms to reach their core customer bases.Fintech firms like Covestor, Betterment, SigFig, and Personal Capital are clearly gaining traction on their own names. But the opportunity for the likes of Fidelity, Vanguard, Schwab, and even the more traditional firms could eclipse all of these current fintech startups put together. That is, of course, if they make the move now, not later.

Contact Us

Centric Digital is no longer active. This site is preserved as an archive. For inquiries, please fill out the form.

© Centric Digital 2025