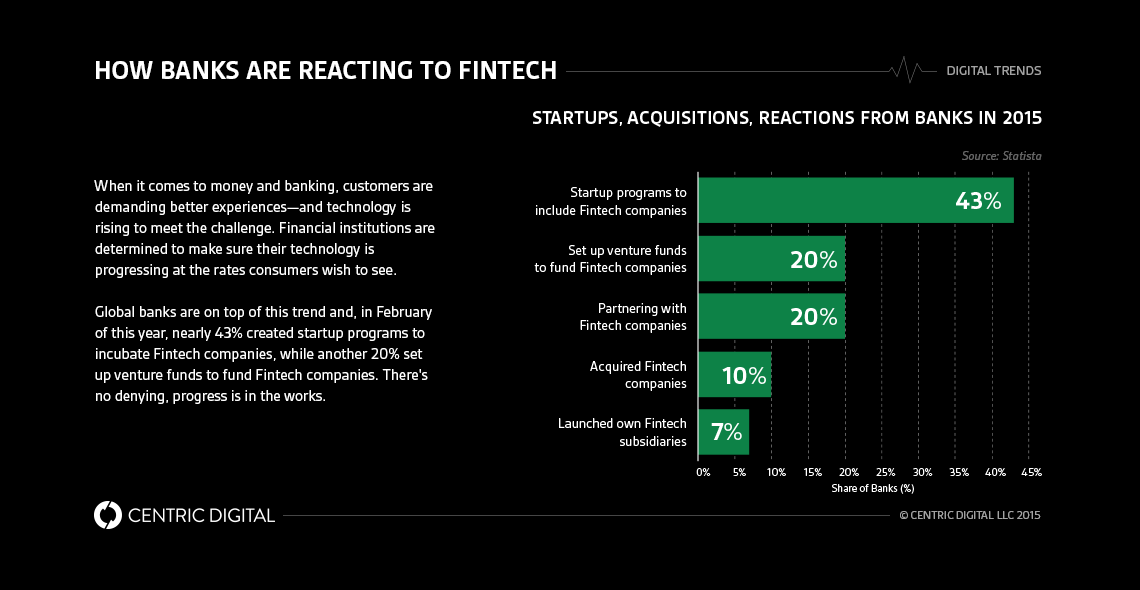

Fintech and innovation might be high on the priority list, but is traditional banking really ready to change their ways?Since 2012, technology has been the top force driving innovation across all sectors. More specifically, a study conducted by Forrester found that the use and experimentation of innovative technologies is taking precedence, with 61 percent of technology leaders and 56 percent of business leaders placing it as the highest technology priority in 2015.The financial industry is not exempt to this trend, and fintech investments and ventures are becoming increasingly popular as independent projects or internal incubators within established financial companies.For the banking industry, fintech represents the cutting edge of innovation, combining the traditional banking services with ever-evolving technological tools.

Fintech Effects

One of the greatest effects fintech has on traditional banking is increased efficiency and cost reductions. Fintech can allow instantaneous communication between branches, departments and staff, and can decrease processing time for things like loans, account openings and other daily tasks. The right technology can also help banks reduce the number of staff required and may even allow for less brick and mortar locations, decreasing overhead.This reduced footprint is another effect of the fintech revolution, as many of the traditional in-bank services are now available online and on mobile devices. With this level of access, consumers simply have less need for physical banks.The traditional approach to banking has also been affected by the public's waning interest in carrying cash. Debit cards, credit cards, and mobile payments are now preferred by a large number of consumers.

How Banks Can Adapt

As fintech banking becomes increasingly popular with consumers, financial institutions have to engage in a digital transformation--taking the focus off of "banks" and placing it on "banking."

Better Use of Big Data

Big data provides a wealth of customer information, but it's worthless if it cannot be accessed, verified, analyzed and distributed effectively. Today, fintech can help banks organize this crucial data so that they can better use it to gain a deeper understanding of their customers. This will allow for more personalized, comprehensive services.As fintech continues to evolve its analytical capabilities, banks will be able to identify and define each customer's experience by their specific circumstances, even before the customer realizes they need a particular service.

Digital Banking

As the tech-savvy Generation X and millennials take over the consumer base, there is a growing demand for fintech services. To these customers, it's important that services and information flow freely between the different channels available to them, from mobile apps to the teller window. Consumers are also looking at emerging technologies, such as mobile payments, that allow them to make purchases and transfer funds with just a few quick taps of the smartphone. They also want to be able to integrate account and payment information into apps directly from their banking institutions.But behind the convenience of digital banking, consumers want to know that their transactions and account information are protected by top-notch security measures. Beyond the two-step authentication process that has become the standard for financial services technology, banks must implement new ways of thwarting digital threats. For example, cyber security pioneers such as BehavioSec are creating interesting new programs. These programs create unique mobile-device security profiles based on unfalsifiable formation such as the force, angle, and speed by which users hit their touchscreen.

A Consumer-Focused Approach

The underlying theme of this evolutionary push is customer-centricity. In the future, banks will find that making the needs of their clientele a top priority will be key to increasing customer satisfaction and loyalty--as well as revenue. Smart fintech will allow banks to provide more holistic services, from traditional offerings such as loans and checking accounts, to budgeting and helping customers make prudent purchasing decisions.

Contact Us

Centric Digital is no longer active. This site is preserved as an archive. For inquiries, please fill out the form.

© Centric Digital 2025