With investment in the FinTech craze growing at a mind-blowing rate, how will the big banks respond? Their next step could define the future of finance on a global level, and that’s why they need to bring it all in-house.FinTech — shorthand for financial technology — is one of the fastest growing industries in the world: investment in this developing field jumped from $930 million in 2008 all the way to $4 billion in 2013. Think that’s impressive? Well, in just the next 365 days, investment skyrocketed up over $12 billion. Now that’s an industry on the rise.According to Accenture, 40% of all FinTech-related venture capital deals made in 2014 were first-round investments in very early-stage, mostly startup companies. FinTech markets are popping up and growing globally at a remarkable rate, most recently in places like Sydney and Hong Kong, and banks are trying to figure out the best way to keep up with the burgeoning market.

Investing in New Trends

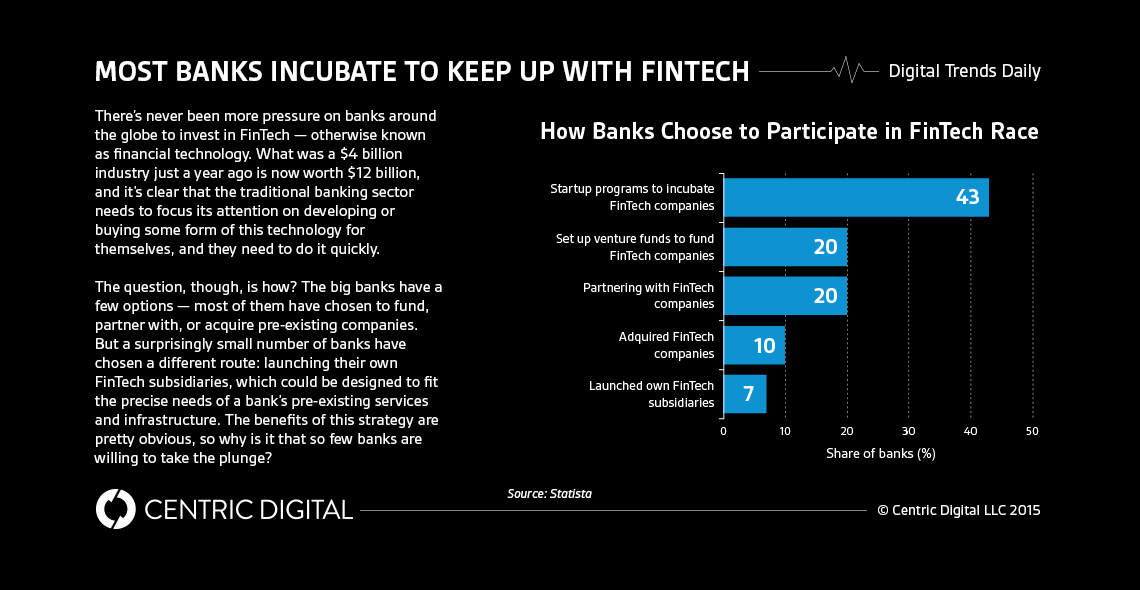

Naturally, banks around the world are feeling increased pressure to show they’re in step with the trend, though the approaches to this initiative are widely varied. The majority choose to outsource, either by initiating programs that incubate individual FinTech companies or by launching venture funds for them.This way, they can access the software and technology another company has already developed without necessarily having to invest their own time and money into the product itself.Surprisingly, only 7% of global banks have launched their own FinTech subsidiaries, and it’s unclear whether this is due to a hesitance to jump into a brand-new market or merely an effort to save money — after all, acquiring or merging with a pre-existing company certainly sounds like a simpler solution.Another 10% of banking and financial services companies have chosen acquisition, and 20% have opted for a more loosely-defined partnership. There’s nothing inherently wrong with these options, of course, but it begs the question: why not create your own proprietary financial technology?

Tailoring Your Technology

The benefits of investing in FinTech in some way are indisputable — they help banks develop faster and cheaper services while simultaneously making themselves an even more essential part of their customers’ daily lives, and I’m talking about both individual people and institutions.The banks that add proprietary FinTech software and services to their daily operations are the ones that will provide smoother operations, better financial security, and, as a result, happier customers that stick around for the long haul.Acquiring a FinTech company works, to be sure, but many have expressed concern over the details of the acquisitions and the speed at which banks can adapt to and successfully implement new technology.To say that working new software and tech services into a well-established bank’s business model is challenging would be an understatement — this process can’t be done quickly or carelessly, or else the entire infrastructure could crumble.I can’t help but think that big banks should consider the more ambitious route — launching their own internal FinTech subsidiaries or programs rather than spending valuable time, money, and resources outsourcing them. If banks want software and technology to work seamlessly with their already-established operations, then why not develop it themselves?Banks shouldn’t have to compromise to get the financial tech that they want and need, or to provide the services that are in increasingly high demand. They certainly have the funds to do it — it’s time that they created something of their own.

Contact Us

Centric Digital is no longer active. This site is preserved as an archive. For inquiries, please fill out the form.

© Centric Digital 2025